Middle East escalation ahead of key US CPI data

Jamie Dutta >

Jamie Dutta >

Jamie Dutta is a Market Analyst for Vantage. He comes with extensive experience as a full-time trader and financial market commentator, having worked as a trader in top tier investment banks and trading houses.

* US says Iran blockade to start on Tuesday evening, and to be hit ‘very hard’

* Saudi Arabia intercepts Houthi missile attack launched in retaliation

* Brent crude jumps 10%, USD and Treasury yields gains, stocks mixed

* Semiconductors crater, SpaceX stock falls over 4% closer to $135 IPO price

FX: USD pushed higher and closed on its highs for the day after the Dollar Index had been consolidating its previous upside breakout from mid-June. Prices had bounced off the top from late March at 100.64. The greenback initially moved higher on the ramp up in Middle East tensions over the weekend, before gains were reversed into the US session. But President Trump hit the wires saying the US will blockade the entire Iranian coastline and assume Hormuz control, which caused risk-off, yields and oil prices to jump, with Brent rising nearly 10% on the day. Fed Governor Waller struck a hawkish tone saying firm core inflation would force the Fed to consider a near-term rate hike.

EUR fell and settled on its lows for the day in a bearish sign. The multi-month bottom from late June sits at 1.1324. the sharp rise in energy prices has ended last week’s corrective euro rally. European gas inventories are also low as a heatwave hits the region. The recent rise in ECB tightening expectations is offering the single currency fundamental support, with December now priced for a cumulative 37bps of rate hikes, from 30bps at the start of the month.

GBP was mid-pack among its peers as cable moved down away form the 50-day and 200-day SMs at 1.3387 and 1.3394. The data calendar is limited ahead of Thursday’s monthly GDP, industrial production, and trade figures for May. Near-term focus is shifting from future PM Burnham’s anticipated July 20 arrival and toward his fiscal plans for the Fall budget and appointee of Chancellor. Options markets aren’t currently pricing in too much worry over this.

JPY weakened as the major traded above the previous major high at 161.95. Official action (both alleged and verbal) remains the key risk for the yen as market participants assess the government’s willingness to defend against major gains above the 162-162.50 range. Some banks are talking about intervention ahead of the public holiday next Monday, similar to what happened in 2024.

US stocks: The S&P 500 lost 0.78% to close at 7,517, the Nasdaq closed down 1.88% at 29,264 and the Dow Jones settled lower by 0.26% at 52,499. Energy was obviously the big outperformer jumping over 3.1% with five defensive sectors also in the green. Tech was the big laggard, losing over 2% with Communication Services and Industrials the next worst off. The weakness in Technology was driven by sharp losses in memory names and semiconductor stocks, with the SOXX down 5% amid concerns surrounding SK Hynix’s upcoming earnings. The stock also gave back some of Friday’s gains following its US listing as the Seoul listing tumbled over 15%.

Asian Stocks: Futures are red. APAC stocks were lower after military strikes between the US and Iran over the weekend. The ASX 200 saw underperformance in tech, mining and materials, though financials offset some losses. The Nikkei 225 retraced after hitting 69,000 with higher oil prices impacting Japanese exporters. The Shanghai Comp and the Hang Seng struggled though downside was limited in Hong Kong.

Gold slid close to 3% as prices looked to be heading towards recent lows just below $4,000. Treasury yields jumped on the back of higher oil prices and fears of Fed rate hikes. The chance of a July move increased from 33% to 41%.

Day Ahead – US CPI

The June US inflation report could prove to be one of the most important market events of the month. Markets are looking for fresh clues on whether inflation is beginning to cool again, or higher prices are becoming more persistent. Oil prices surged during the geopolitical tensions before retreating following improved relations between the US and Iran, leaving investors to assess how much of that earlier energy shock has filtered through to the wider economy. Under new boss Warsh, policymakers at the Fed are now keenly focused on restoring inflation to their 2% target, and any signs that price pressures are becoming “sticky” could reinforce expectations that interest rates remain higher for longer.

Consensus forecast headline CPI to fall 0.1% month-on-month in June after rising 0.5% in May, with the annual inflation rate forecast to ease to 3.9% from 4.2%. Core inflation, which strips out volatile food and energy prices, is expected to rise 0.3% month-on-month, while the annual rate is forecast to remain unchanged at 2.9%. The Fed pays particularly close attention to whether temporary price shocks begin spreading through the wider economy in what economists call “second-round effects”. These occur when higher energy costs feed into transport, wages and everyday goods, making inflation much harder to bring back under control. So far, there has been little evidence that this process has taken hold, but June’s data will provide another important test.

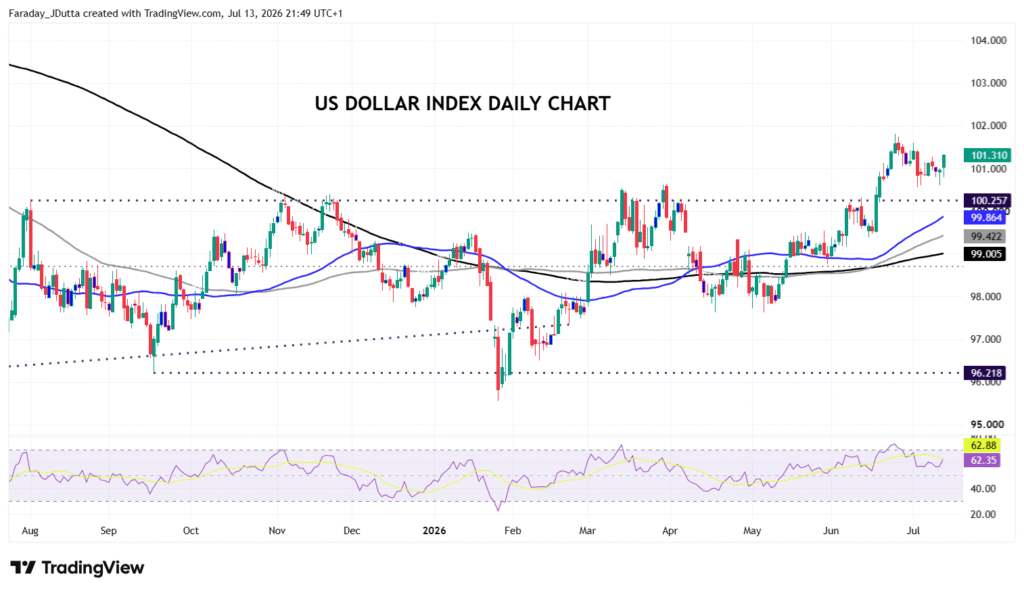

Chart of the Day – Dollar Index upside break?

The recent decline in oil prices should help lower headline inflation, although investors will also be watching this week’s Producer Price Index (PPI) data released on Wednesday for signs of cost pressures further up the supply chain. There’s roughly a 42% chance of a Fed rate hike at the end of July meeting, with around 35bps in total for 2026. In other words, that means a 40% chance of two 25bps rate hikes. If inflation comes in hotter than expected, markets are likely to increase bets that the Fed will keep policy restrictive for longer and potentially hike rates soon. That should support and lift the US dollar. A softer reading, however, would reinforce the view that the recent rise in inflation was largely driven by temporary – whisper it quietly, ‘transitory’ – energy costs. That outcome could ease pressure on policymakers, support risk appetite and hurt the buck. Obviously, the current jump in oil prices could see markets look through this report to some extent. The Dollar Index has been consolidating bullishly in recent days with buyers looking to the recent highs and resistance around 101.80.