Sentiment improves as semiconductors rebound

Jamie Dutta >

Jamie Dutta >

Jamie Dutta is a Market Analyst for Vantage. He comes with extensive experience as a full-time trader and financial market commentator, having worked as a trader in top tier investment banks and trading houses.

* US strikes Iranian railway bridges on route to city of Khamenei’s burial

* US says Lebanon, Israel enter next phase of Hezbollah disarmament deal

* Brent crude slips as traders reassess Hormuz risks

* Semiconductors gained ahead of SK Hynix $28 billion share sale

FX: USD was lost ground for a second straight day even amid heightened geopolitical tensions between the US and Iran. There were more strikes and yet markets seem willing to fade any greenback gains despite elevated uncertainty which would typically give the buck a bid. Later on, risk sentiment improved after President Trump said Iran had reached out to the US and wanted to make a deal, easing concerns over a further escalation that could threaten energy infrastructure. Wednesday’s FOMC minutes didn’t give us anything new, with the more hawkish tilt to the new Fed evident. The spotlight turns to next week’s CPI and PPI data which is now ratesetters key focus.

EUR has held up well considering higher oil prices and found buyers again on Wednesday. The outlook for relative central bank policy is offering the single currency support as markets reprice the ECB outlook in light of renewed hawkishness and a resurgence in geopolitically driven energy price gains. Traders are currently pricing in about 35bps of rate hikes by year-end, a considerable increase over the past week or so. The latest minutes also backed this sentiment. The July top sits at 1.1472.

GBP continued to trade around the 50-day and 200-day SMAs at 1.3403 and 1.3395. Sterling is outperforming its major peers this week, copying its performance at the start of the Gulf crisis in early March. The sterling money market curve adjusts more than in the eurozone and elsewhere as markets price in more tightening due to the oil price rally. The current domestic politics picture is also underpinning some support for the pound.

JPY pulled back modestly from recent highs, with the recent long-term multi-decade peak at 162.83. Reports of an acceleration in the BoJ’s tightening path may offer the yen support, but rate expectations remain relatively muted into the late July rate decision with markets still pricing only about 25bps of tightening by December.

US stocks: The S&P 500 added 0.81% to close at 7,544, the Nasdaq closed up 1.62% at 29,727 and the Dow Jones settled higher by 0.27% at 52,492. Tech and Consumer Discretionary led the gainers with only four sectors in the red, including Consumer Staples and Energy, which lagged on falling crude oil prices. Semiconductors gained ahead of SK Hynix’s giant share sale. The SOXX semiconductor index rose more than 3%. PepsiCo fell 3.3% as revenue declined while sales volumes rose. The former were hurt by tightening consumer budgets and the giant snack maker expects higher input cost inflation in the second half. Delta Air Lines report earnings later today.

Asian Stocks: Futures are mixed. APAC stocks opened with solid gains and proved resilient in keeping most of those. The ASX 200 softened as metals and mining weakness offset energy’s outperformance. The Nikkei 225 was the only major index printing gains, boosted by Tokyo Electron and its ability to cut chip gear delivery times by 50%. The Shanghai Comp and the Hang Seng opened with modest gains but partially retraced those, with one eye on IPOs for the Hang Seng.

Gold firmed as the dollar and yields eased back. Crude came of recent highs after hitting the 200-day SMA.

Day Ahead – Canada Jobs

Consensus sees the headline print at 10k, down from the stellar 88k growth in May. Hiring intentions have been mixed in recent months, with mean reversion likely to offset the previous month’s outsized gain. Wage growth is expected to edge up to 3.6%, reversing only a small part of May’s slowdown. The recent Bank of Canada minutes revealed officials saw slack in the labour market, with the economy still operating in excess supply. Markets currently give a coin flip chance of a rate hike by year-end.

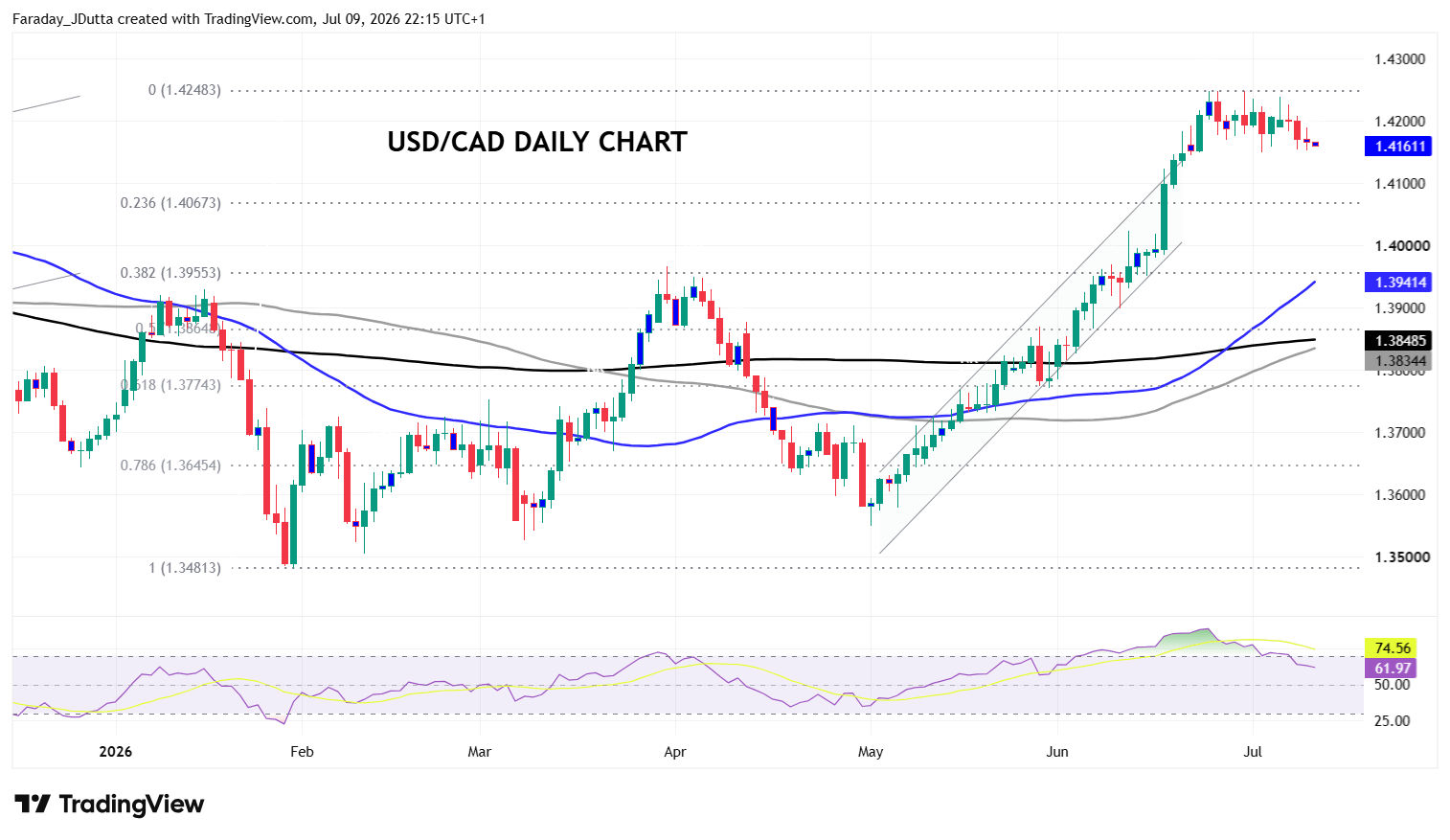

Chart of the Day – USD/CAD pauses

USD had been on a tear since the start of May versus the loonie, rising from a low of 1.3549 to a high in late June at 1.4248. The near-perfect bull channel, with short, sharp higher highs and higher lows pushed the major into extremely overbought territory after ten straight days of gains. The 1.4250/00 range should offer firm resistance to a further USD advance. A break under support at 1.4150 would be a bearish signal and prompt the pair to test important support around 1.4067/80.