Chip stock volatility continues, bonds and gold weak

Jamie Dutta >

Jamie Dutta >

Jamie Dutta is a Market Analyst for Vantage. He comes with extensive experience as a full-time trader and financial market commentator, having worked as a trader in top tier investment banks and trading houses.

- US commences fifth consecutive night of military strikes against Iran

- Google Gemini launch delayed as tech falls short of internal goals

- Netflix Q2 earnings results in-line with expectations, stock drops

- SpaceX slide below IPO price risks confidence test in blockbuster IPO

Forex

USD found a bid and outperformed though prices traded in a relatively small range. That likely means FX volatility could be waning again after Monday’s post-weekend bounce. This week’s soft CPI data has put paid to a more prolonged greenback rally so far, while Wednesday’s PPI figures were also muted. That said, one data point does not make trend, which is essentially what new Fed boss Warsh warned in his first semi-annual testimony on Tuesday. Otherwise, yesterday’s data was mixed with retail sales rising modestly in June potentially boosted by Amazon Prime Day and the FIFA World Cup, while initial jobless claims fell.

EUR traded in a narrow range, printing an ‘inside day’ candle where the high and low for the day are inside the prior day’s range. That typically denotes some indecision between buyers and sellers. The world’s most popular currency pair has been trying to build a base around 1.14 but likely needs oil and especially gas prices to fall. The latter are more impactful for the zone’s terms of trade. However, the recent significant narrowing in EZ/US short-term spreads since the start of July should underpin support for the euro.

GBP was a modest underperformer, which came on the back of stellar gains on Wednesday. UK GDP outperformed, though economists say this follows other instances of strong growth at the start of the year ahead of slowing momentum later on. See below for more.

JPY continued to consolidate just below previous highs with the recent peak at 162.83. That sits just above the long-term top from July 2024 when we saw major intervention at 161.95. A former finance official said the BoJ was behind the curve and needed to raise rates more rapidly to support the yen.

Stocks

US stocks: The S&P 500 lost 0.51% to close at 7,534, the Nasdaq closed down 1.62% at 29,026 and the Dow Jones settled lower by 0.2% at 52,554. Looking beneath the red headline indices, underlying market breadth was actually more constructive. The equal-weight S&P 500 rose around 0.75%, while a slight majority of sectors finished in positive territory. Consumer Staples led the gains, with Health Care and Real Estate also outperforming. By contrast, Communication Services, Technology and Industrials lagged, highlighting that much of the weakness was concentrated within AI-related names rather than the broader market.

The spotlight was on more volatility in chip stocks after TSMC posted its fifth straight quarter of record earnings earlier in the day. But that wasn’t enough to help the broader sector, with the SOXX index sliding over 4%. On the flip side, Apple hit more record highs for a second straight day, pushing its market cap up to $4.8 billion. Notably, the Cupertino-based giant has kept its AI spending in check, in stark contrast to the hyperscalers who are spending $100s of billions on AI infrastructure. Apple is outperforming the Nasdaq currently by more than 13% for the quarter. SpaceX fell more than 3% and below its IPO price as short sellers eyed its latest earnings and locked up shares, which would be ready to offload soon. Alphabet fell 4.4% after reports it had delayed the launch of Gemini 3.5 after the model failed to meet internal performance targets.

Netflix reported after the closing bell, with second-quarter revenue and earnings in line with estimates. Its revenue increase was attributed to membership growth, pricing and higher advertising revenue. The streaming giant said its engagement is “healthy” following recent reports of a slowdown for the metric. The stock was down 8% after hours.

Asian Stocks: Futures are mixed. APAC stocks were also mixed with the risk mood dampened by the semiconductor sell-off Stateside. The ASX 200 was muted with mining losses after BHP reported lower output. The Nikkei 225 eased back with the tech-heavy index impacted by chip stock selling. The Shanghai Comp and the Hang Seng were mixed with disappointing loans data hurting the mainland while Hong Kong rallied amid strength in hyperscalers following reports that US companies were increasingly adopting open-weight Chinese AI models.

Gold

Gold gave back gains from the prior two days as Middle East tensions continued to support energy prices and keep inflation risks elevated. That meant higher Treasury yields and dollar amid some hawkish Fed commentary.

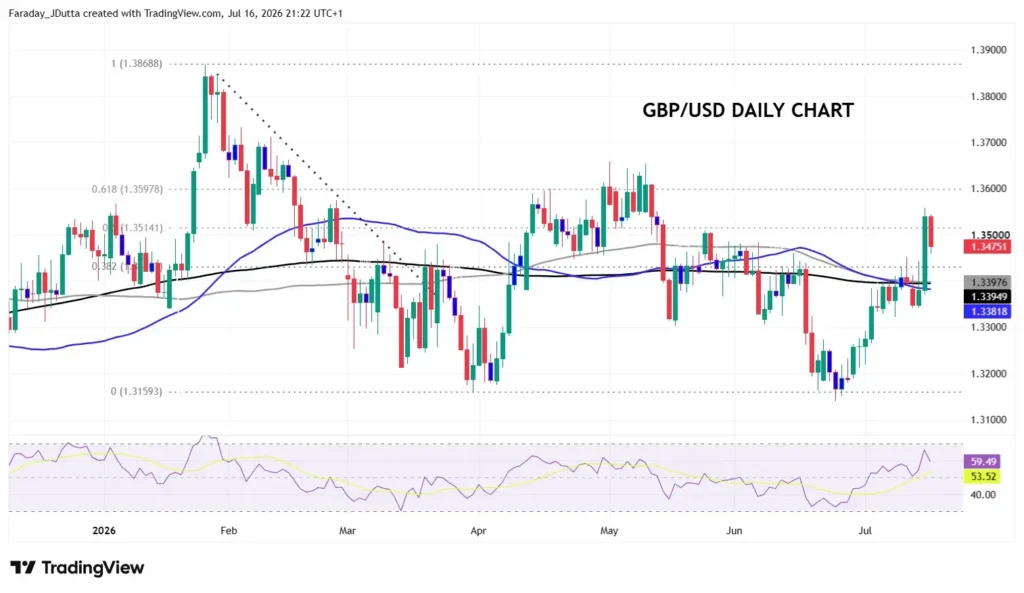

Chart of the Day – Whippy GBP price action

A sharp move (and then small reversal) was seen in sterling on Wednesday and Thursday, which was likely due to a couple of key reasons. Position adjustment, with the shortest sterling positions by speculators being seen since 2017, have been squeezed considerably. The FT also ran reports that current Home Secretary Mahmood is now predicted to be the new Chancellor. She should be more right leaning, less divisive and less fiscally expansive; certainly more than heavy prior favourite Ed Miliband, even though little is known about her economic tendencies. Much will be revealed when PM Burnham takes the hot seat on Monday, while important UK CPI and jobs data will also be released next week.

Sterling burst higher after consolidating around the long-term 50, 100, and 200-day SMAs at 1.34. This has livened up the charts and sets the pound up for a further extension of the early July bull reversal. The fresh short-term cycle high and a bullish alignment of trend oscillators suggest minor dips are a buy and that GBP gains can extend towards a retest of 1.3650 at least if bulls keep above 1.3450 in the near-term. EURGBP traded back from Wednesday’s one-year low but technical trends also look positive for the pound overall, especially if the cross keeps below 0.8479, a long-term major Fib level.