Gold, black gold, bond yields battered as Micron soars

* Crude oil hits fresh lows below $70 as tankers transit Strait of Hormuz

* Dollar rises to 13-month high on Fed hike bets

* S&P 500 & Nasdaq mixed as tech weighs, Dow Jones up on defensive rotation

* Micron tops Q3 earnings estimates, offers better than expected guidance

FX: USD pushed up to more cycle highs at 101.80. The tech-led stock sell-off has spilled into FX with risk-off currencies like the dollar, yen and CHF outperforming high beta ones like AUD, NZD, SEK and NOK. (For your guide, AUD has the highest correlation in G10 with the Philadelphia Semiconductor index, meaning downside risks remain elevated in the near term if AI valuation concerns persist). We are getting ‘toppy’ in this dollar move, both on the charts and perhaps with Fed rate hike pricing as markets price around a 40% of a 25bps rate rise at the July FOMC meeting. Crude prices tumbled to their lowest levels since the war began, allowing for US yields to retreat a little lower.

EUR broke down further away from the mid-March 2026 low at 1.1410. Risk aversion continues to help the greenback. There was more ECB speak with Chief Economist Lane warnings that inflation is set to stay above 2% for some time. We got similarly modestly hawkish and expected comments from Schnabel too. This could be a push back against President Lagarde’s recent chatter, with Lane better reflecting ECB consensus.

GBP was mid-pack as it posted a new year-to-date low, below the late March trough at 1.3159. EUR/GBP traded just above the 200-week moving average @ 0.8596, with a big support zone on the daily chart around 0.8611/21. There wasn’t much domestic news, but lingering positivity from the incoming Burnham premiership.

JPY continued to consolidate just below the key long-term resistance level at 161.95, with the yen as the best performing major currency so far this week. BoJ Governor said there are risks that underlying inflation may overshoot 2% but Japan’s economy is recovering moderately with some weakness. The BoJ minutes stated that the bank must maintain its stance of proceeding with further rate hikes if the economy and prices move in line with forecasts.

US stocks: The S&P 500 lost 0.1% to close at 7,358, the Nasdaq closed down 0.43% at 29,220 and the Dow Jones settled higher by 0.35% at 51,854. Six sectors gained with breadth strong, but the continued tech weakness weighed on the broader indices, leaving SPX and NDX in the red. Industrials, Utilities and Healthcare led the gainers. The underlying growth and earnings picture remains solid, and investors are rotating across equities rather than engaging in a broad-based sell-off. Positioning and the momentum in certain tech areas has been extreme since late March so corrections are healthy and logical, into defensives and other areas. Major stock updates included Cerebras sinking 19% on expected declines in gross margins, Alphabet (-0.3%) to replace Verizon in the Dow Jones, and OpenAI and Broadcom (+0.51%) unveiling an LLM-optimised intelligence processor. Micron released its latest earnings after the close with the stock up more than 15%. Soaring prices from the memory chip crunch led to a quadrupling of revenue. The company’s market cap raced past $1 trillion in recent weeks with the stock price up about 700% over the past year.

Asian Stocks: Futures are mixed. APAC stocks traded mixed on Wall Street’s. The ASX 200 traded rangebound with tech and defensive strength offset by mining and energy losses. The Nikkei 225 dipped below 70,000 with one eye on the BoJ minutes which showed members continued to advocate for more rate hikes. The Hang Seng and Shanghai Comp were muted with some focus on the World Economic Forum where Premier Li said China’s economy shows resilience and it remains committed to opening up to accelerate the large-scale application of new technologies.

Gold fell for a fifth straight day as it broke the long-term low from earlier in the month at $4,023 to a fresh trough at $3,959. Again, the stronger dollar and higher real yields are hurting the non-yielding asset as the Fed is potentially keeping rates higher for longer.

Day Ahead – Australia Jobs, US Core PCE

The headline Aussie employment figure is expected to rebound to 30k from a decline of 18.6k previously, with the unemployment rate falling one-tenth to 4.4%. April’s employment report surprised on the downside, with the weakness potentially linked to abnormal seasonality as it captured the full Easter long weekend. Jobs growth is slowing from roughly 30k-a-month pace seen at the start of the year. However, the RBA appears less concerned about the labour market than inflation, with Governor Bullock recently stating that “the labour market is still a bit tight at the current unemployment rate”. Markets are currently pricing 37bps of hikes by year-end.

The Fed’s favoured inflation gauge is predicted to remain steady at 0.4% m/m and rise to 3.4% y/y. These figures are for May so could be deemed stale as oil prices have fallen sharply in recent weeks. The hawkish Fed meeting under new Governor Warsh stressed price stability, as the FOMC has missed its inflation target for the past five years. This clear hawkishness of the Fed and the enhanced focus on inflation will make price data even more important ahead. We are asking ourselves if May is now the peak in inflation as energy prices fall sharply?

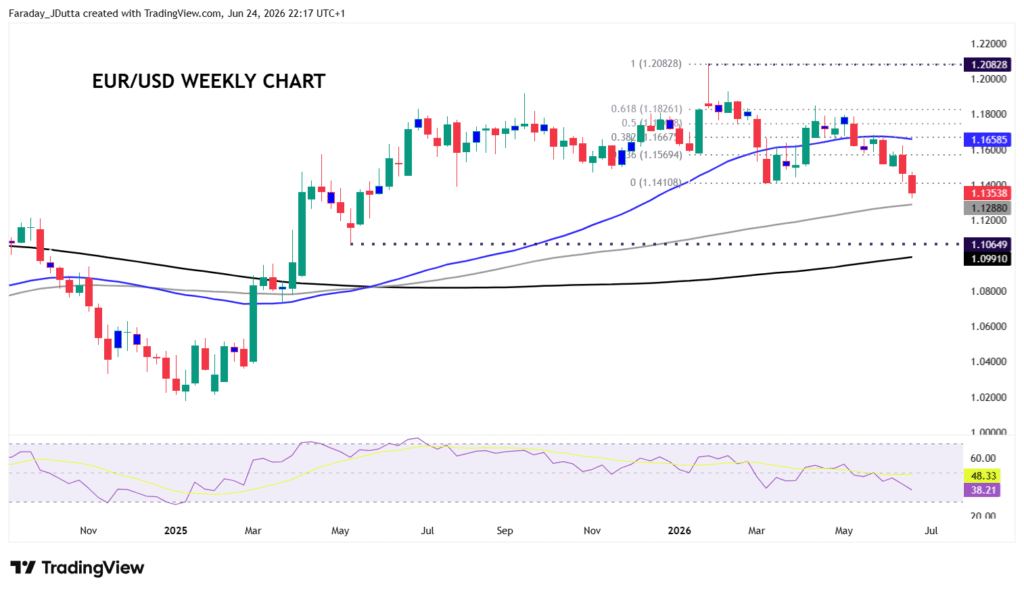

Chart of the Day – EUR/USD breakdown

The world’s most popular FX pair has been falling down since the middle of the month. Bearish momentum took it through the psychologically important and technically relevant 1.14 level and prior 2026 low at 1.1410, reaching levels last seen in May 2025. There is not much near-term support aside the 100-week SMA at 1.1288, ahead of the mid-1.12s and nothing major ahead of 1.10. Momentum remains bearish but is oversold, with the daily RSI now around 25. Prices hit a low of 1.1324 intraday before paring losses. As we mentioned in the weekly, the region’s soft PMIs contrasted with a small bump in the US surveys. This reinforces the outlook for relative central bank policy which remains a headwind for the single currency, largely driven by the recent hawkish re-pricing of Fed expectations as those for the ECB have remained largely unchanged.