Soft NFP pushes dollar down, JPY surges on likely intervention

Jamie Dutta >

Jamie Dutta >

Jamie Dutta is a Market Analyst for Vantage. He comes with extensive experience as a full-time trader and financial market commentator, having worked as a trader in top tier investment banks and trading houses.

- US hiring slows sharply curbing recent job market momentum

- US offers to unfreeze Iranian funds to open Straits of Hormuz

- Dollar slides after soft jobs report, stocks mixed as tech toils again

- Yen rebounds after 40-year lows amid intervention-type price action

Forex

USD got sold as it suffered its worst day in two months. Initially, suspected intervention in USD/JPY moved the dollar sharply lower in the European session. The softer-than-forecast NFP headline print of 57k against the consensus 115k saw further selling, though the jobless rate unexpectedly ticked one-tenth lower to 4.2%. Obviously, it is only one data point and new Fed Chair Warsh will want to see a series of reports to measure if this is a temporary soft patch or a one-off amid solid labour market data. Money markets reined in Fed rate hikes with around 30bps now priced in, versus 36bps before the NFP data.

EUR rose to 1.1472 before paring gains as the NFP report and likely yen intervention saw the dollar lower. Softer eurozone inflation figures on Wednesday raise questions about whether the ECB needs to follow up with a hike in September, with markets currently pricing in around 14bps for that meeting. However, economists say inflation could pick up over the coming months as many government energy subsidy measures expire at the end of June.

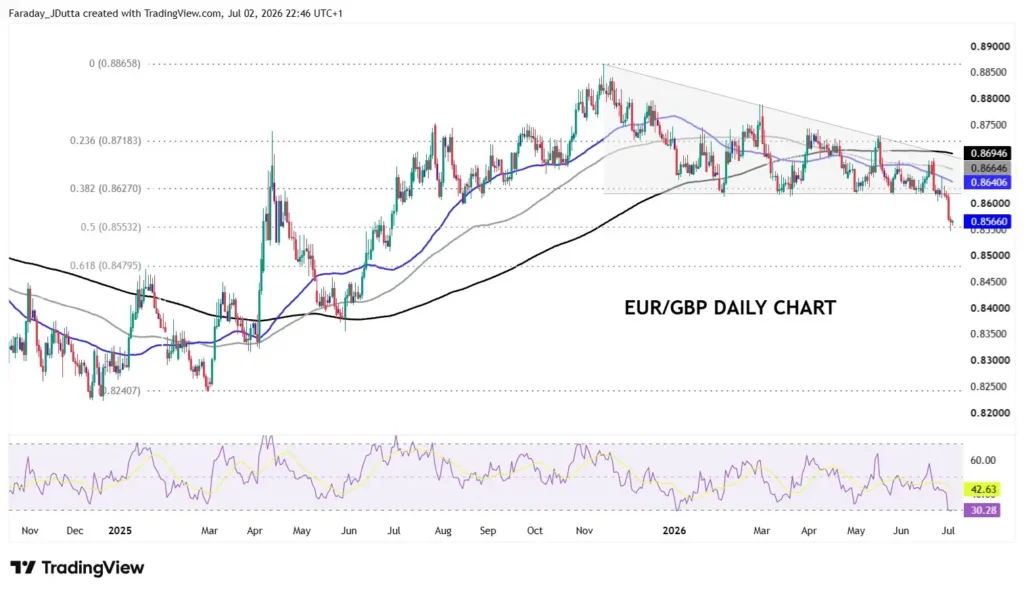

GBP rose sharply for a fifth day in six as prices neared the 200-day SMA at 1.3396 and 50-day SMA at 1.3409. PM Burnham said he will stick to the Labour manifesto on tax; while he has not made up his mind on who his chancellor will be. EUR/GBP fell for a fifth straight day, lower after its big breakdown on Tuesday through the key 0.8620 level. See more below on this popular cross.

JPY was the big outperformeras the European session saw huge selling in the major. The pair fell from 162.20 to 161.12 very sharply, though the drop pared back some of its losses. This came after the fresh high at 162.83 on Wednesday and much chatter about when intervention would come. The move comes after Reuters reported that Japan would abandon its habit of warning the markets of intervention. The aim of this is to squeeze speculators and increase the cost of betting against the yen. Of course, the weaker than expected NFP headline helped yen strength versus dollar weakness. Will the MoF capitalise on thin liquidity over the US holiday today with more selling?

Stocks

US stocks: The S&P 500 lost 0.01% to close at 7,483, the Nasdaq closed down 1.61% at 29,329 and the Dow Jones settled higher by 1.14% at 52,904. Market breadth was more constructive than the headline indices suggest. Most sectors finished higher, led by the traditional defensive sectors of Health Care, Consumer Staples and Utilities, while Technology, Consumer Discretionary and Communication Services sectors were the clear laggards. Tech selling reflected a continuation of Wednesday’s weakness following the Meta disruption. It reversed its previous session’s gains, however, with lows seen after CEO Zuckerberg said AI agent development had not accelerated in the way the company had expected. Meanwhile, memory stocks remained under pressure, with the SOXX index down 5.4% and names like Sandisk down 141.15 and Seagate off 10.4%. Apple bucked the trend, up 4.8% but Tesla plummeted more than 7% despite stronger-than-expected delivery numbers. Some profit-taking and position squaring was likely the big driver ahead of the long Independence Day weekend, with US markets closed on Friday.

Asian Stocks: Futures are mixed. APAC stocks were mixed due to tech losses Stateside. The ASX 200 was rangebound with financials strength offset by losses in tech and utilities. The Nikkei 225 was modestly whippy with some initial selling, a bounce back and then more weakness. The Shanghai Comp and the Hang Seng were mixed though the latter local tech and autos were solid.

Gold

Gold bounced off the $4,000 level though still remains in consolidation mode. Bugs really have to get above the 200-day SMA at $4,460 to break the downtrend. We note the 50-day SMA has moved below the 200-day which is a bearish death cross, but the timing can sometimes be variable.

Chart of the Day – EUR/GBP consolidates breakdown

A big bearish triangle in EUR/GBP looks to have finally cracked. The pair has seen a series of lower highs while prices have found support around 0.8620 on numerous occasions this year. There’s not been one obvious catalyst which saw the breakdown on Tuesday but some unwinding of stale sterling short positions, after asset managers had been running some large sterling short positions seems likely. At the same time, it is expensive to be short sterling, where one-week rates are around 3.80%, and with volatility falling, some position liquidation is obvious. UK domestic politics has also calmed down, though focus is on the appointment of the new Chancellor which could be left-leaning Ed Miliband. Prices are now just above the midpoint of the 2025 low to 2025 high at 0.8553. The next major Fib below sits at 0.8479, in a support zone with the 38.2% retracement level at 0.8627 and subsequent breakdown.